The New Regulatory Sanitation Room for the Venezuelan Hydrocarbons Sector: The General License 52

Source: OFAC

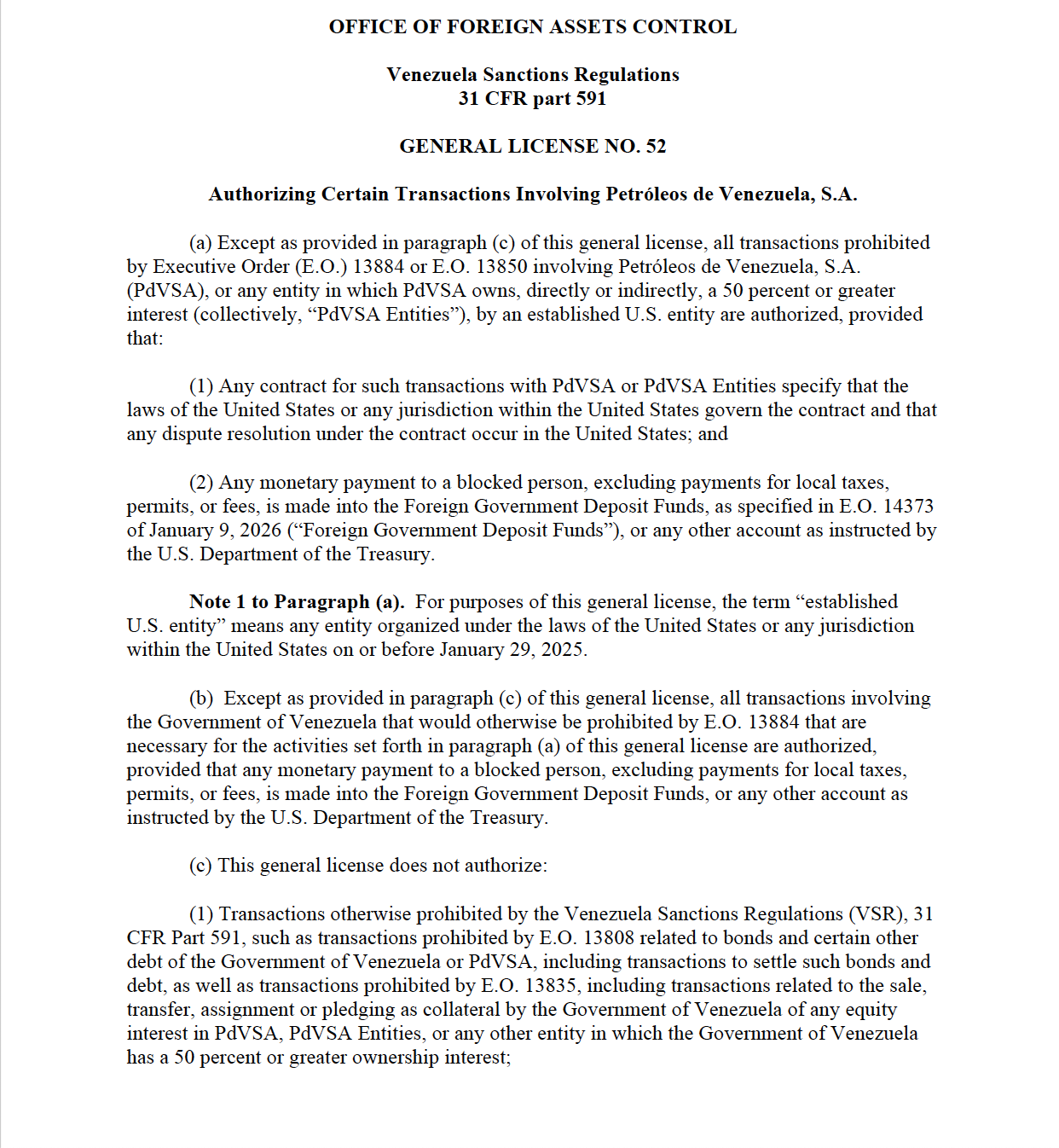

On March 18, 2026, OFAC issued General License 52 (GL52). So far, this is the most important license granted in the Venezuelan hydrocarbons sector, defining policies that were previously unclear.

In summary, GL52, as clarified by the new FAQs. includes three policies: (i) a broad authorization for any prohibited transaction with PDVSA in favor of “any established U.S. entity,” (ii) a “regulatory sanitation room” that ratifies the U.S. Government’s (USG) control over all of Venezuela’s incomes, and (iii) a renewed protective framework regarding the creditors’ claims

The broad authorization

Section (a) of GL52 authorizes all transactions prohibited by the economic sanction regulations involving PDVSA or any entity in which PDVSA “owns, directly or indirectly, a 50 percent or greater interest”. The authorization only applies to established U.S. entities, that is, “any entity organized under the laws of the United States or any jurisdiction within the United States on or before January 29, 2025”.

The authorization applies to all prohibited transactions, except those included in section (c) regarding creditors’ claims. Hence, GL52 covers any oil and gas operation involving PDVSA (upstream and downstream) for established U.S. entities, expanding the scope of the prior general licenses, including General Licenses 49A and 50A. Particularly, section (b) states that the authorization covers any transaction necessary for the activities authorized in section (a).

In that regard, FAQ 1245 confirms the broad scope of the new license, including activities such as the “lifting, exportation, reexportation, sale, resale, supply, storage, marketing, purchase, delivery, or transportation of Venezuelan oil”, and the “entry into new investment contracts for exploration, development, or production activities in the oil, gas, or petroleum products sectors of Venezuela”.

Therefore, a rational interpretation of those general licenses could be based on the following distinction:

- Any oil and gas company that qualifies as an established U.S. entity will be covered by the broad authorization under GL52, without having to rely on other OFAC licenses. Hence, those firms are authorized to negotiate new contracts with PDVSA (regardless of GL49A) and to conduct oil and gas operations (regardless of GL50A). The firms included in GL50A could operate under the scope of GL52 through an affiliate that qualifies as an established U.S. entity.

- Oil and gas companies that do not qualify as established U.S. companies will not be covered under GL52. Hence, any transaction with PDVSA should be covered by any of the general licenses issued, including GL49A.

In any case, GL52 ratified the boilerplate condition that any oil and gas contract must “specify that the laws of the United States or any jurisdiction within the United States govern the contract and that any dispute resolution under the contract occur in the United States”. This provision creates unresolved tension with the Venezuelan public law.

The regulatory sanitation room

GL52 ratifies another boilerplate condition regarding what we have called the “regulatory sanitation room”: any payment to the Government of Venezuela will be exclusively administered by the USG, in accordance with EO 14373.

Sections (a) and (b) provide that any payment to any blocked instrumentality of the Government of Venezuela should be made into the Foreign Government Deposit Funds, regulated by EO 14373. The only payments excluded are those related to local taxes, permits, or fees.

As a result, any payment owed to the Republic based on the oil and gas “government take”, as well as any payment related to the sale of PDVSA´s own production, will be deposited in Foreign Government Deposit Funds. The USG has the exclusive authority to decide which funds may be transferred to the Government of Venezuela, particularly for conducting exchange operations in the Venezuelan market, thereby providing the Government with the local currency resources needed to cover expenses. This framework causes significant distortions in Venezuela’s fiscal rules and unresolved issues in Venezuelan hydrocarbons regulation.

The final purpose of the Foreign Government Deposit Funds is to isolate Venezuelan oil & gas income (as well as gold income, based on GL51) from any risk associated with the Government of Venezuela, particularly due to poor governance practices.

This “regulatory sanitation room” also isolates the hydrocarbon sector from the influence of Cuba, Iran, North Korea, and China, because the authorization does not apply to transactions involving those actors, as defined in section (c), numerals 5 and 6.

The renewed asset protection measures

One of the issues handled by the “regulatory sanitation room” involves Venezuela’s roughly $170 billion in external debt, as EO 14373 restricted creditors from seizing the Foreign Government Deposit Funds. Subsequently, section (c) of GL52 summarizes the asset protection measures and prohibitions related to the Venezuelan debt:

- Prohibited transactions with the Venezuelan bonds, including those prohibited by EO 13808 and EO 13835. In particular, transactions to settle such bonds are not permitted (numeral 1).

- GL52 also ratifies the prohibition related to the sale, transfer, assignment, or pledging as collateral by the Government of Venezuela of any equity interest in PdVSA”, which is relevant to the collateral over 50,1% of shares of Citgo Holding, Inc. (numeral 1).

- The entry into a settlement agreement or the enforcement of any lien, judgment, arbitral award, decree, or other order through execution, garnishment, or other judicial process purporting to transfer or otherwise alter or affect property or interests in property of the Government of Venezuela, including PDVSA (numeral 2).

- Payment terms that are not commercially reasonable, including debt swaps (numeral 4).

GL52 confirmed that Venezuelan incomes from the oil & gas sector should be prioritized for the purposes outlined in EO 14373 and not used to pay claims by legacy creditors through settlements or seizure measures. In particular, and pursuant to numeral 2 of section (3), GL52 ratifies that the shares of PDV Holding, Inc., as well as those of its Citgo affiliates, cannot be enforced in any judicial process. In this matter, however, a pending issue remains regarding the upcoming expiration, on March 20, of the suspension of General License 5.

In any case, the debt transactions prohibited under section (3) could be authorized by specific OFAC licenses. In that sense, FAQ 1246 clarified that GL52 does not authorize “the sale of certain shares of CITGO that are the subject of Crystallex International Corporation v. Bolivarian Republic of Venezuela”, meaning that a “specific license will be required before any sale is executed in the Crystallex case.