Untangling the Knot of the Venezuela´s Public Debt: Legal Notes on the Reestructuring Announcement

The announcement by Venezuela’s Sectoral Vice-Presidency for Economy regarding the launch of the public-debt restructuring, together with the press release — in English — by the financial-advisory firm Centerview, has generated a range of debates, particularly among economists.

Beyond the economic considerations, there is a legal dimension that should not be overlooked. In essence, the announced restructuring is, first and foremost, a legal process that will be implemented through acts and contracts with legal effects. As a legal process, its analysis must take into account the present conditions of the rule of law in Venezuela.

I do not purport to exhaust all the legal issues raised by the announcement here. In this article, I confine myself to addressing the institutional context and the general principles that flow from it, leaving for another occasion the analysis of the steps that may be expected to follow.

The Eighth Announcement

Since Venezuela unilaterally suspended payments on its financial debt on November 2, 2017, there have been up to seven announcements of an imminent restructuring — or, more precisely, renegotiation — of the debt. Seven announcements that remained nothing more than broken promises.

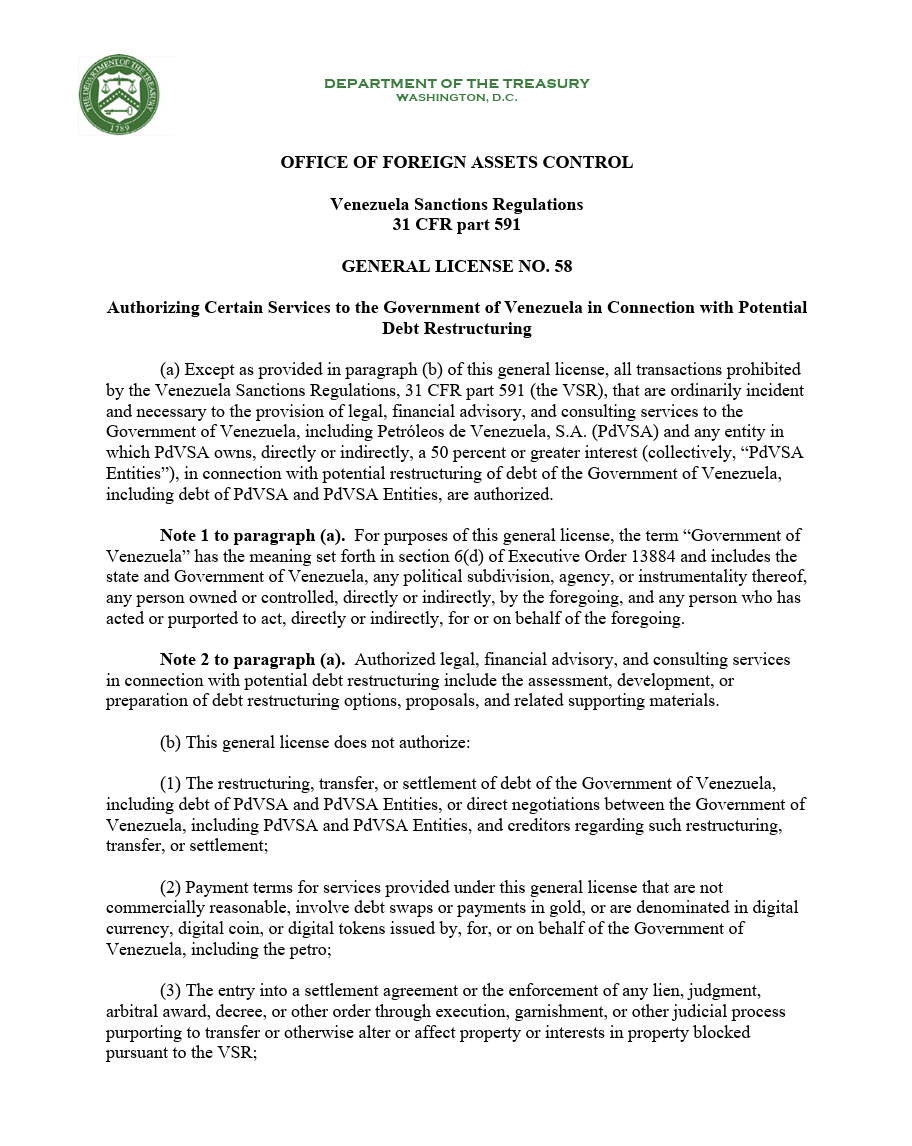

This eighth announcement, however, may differ, as it responds directly to U.S. Government policy toward Venezuela, as reflected in General License No. 58 of May 5, 2026, which I have analyzed here. That license authorized the engagement of advisors to prepare a possible renegotiation of the public debt, although it did not authorize any direct negotiation with creditors.

For that reason, it was only a matter of time before the “interim authorities” announced how they intended to act under that license. The May 13 announcement is, precisely, the official response to General License No. 58.

From this perspective, the communiqué is not surprising; it is a more-than-expected response. It cannot, therefore, be read in isolation from General License No. 58 or from the other policies adopted by the U.S. Government toward Venezuela since January 3, 2026.

The Rationale for Renegotiation: Six Core Objectives

The legal procedure for renegotiating the debt is not exhaustively set out in any single statute. Still, it is governed by the rules, principles, and values of Venezuelan public law, interpreted in light of the applicable international standards. Recently, the standards governing the debt-renegotiation procedure were updated to cover what is referred to as “Step Zero”—the preparatory actions.

General License No. 58 authorizes, precisely, only the actions necessary for that Step Zero. The official Spanish-language announcement sets out the rationale for those preliminary actions, which produce relevant legal effects under the principles of transparency and good faith.

In accordance with the principle of reasoned justification of administrative action, the communiqué presents a rational analysis of the constitutional and economic objectives — in that order — of the renegotiation process, which coincide with previously advanced proposals. Six objectives are worth highlighting.

The first objective is to restore debt sustainability. According to the communiqué, the financial obligations are “unsustainable” — that is, the government is unable to meet them while also fulfilling its other obligations, especially those related to economic and social policy. This is consistent with Articles 311 and 312 of the Venezuelan Constitution.

The second objective is to focus the process on the external debt, which, under Venezuelan law, encompasses pecuniary obligations in foreign currency owed to creditors not domiciled in Venezuela. The domicile criterion can produce distortions, since what matters is the currency of payment. In any event, it can be rational to renegotiate the external and domestic debt separately, as has been proposed before.

The third principle is that the renegotiation of the external debt must be comprehensive and must therefore cover the entire public sector, even though the communiqué mentions only the Republic and PDVSA. The other public entities owing obligations in foreign currency — such as ELECAR (now CORPOELEC) — should be included.

Related to the foregoing, the fourth principle addresses comprehensiveness on the creditor side. Only official creditors — that is, bilateral and multilateral debt — would be excluded, which also matches previous proposals. This implies that the renegotiation would cover all private creditors, including bondholders. It is worth clarifying that none of the communiqués limits the announcement to bonded external debt alone.

The fifth principle is to prioritize fiscal capacity for economic and social policies aimed at Venezuela’s recovery and meeting humanitarian needs. As the communiqué states, the renegotiation is aimed at “placing the economy at the service of the Venezuelan people and freeing the country from the burden of accumulated debt, securing its future and a rebirth of prosperity, justice and equality,” which is consistent with Articles 311 and 312 of the Constitution.

The sixth principle concerns the policy tools for restoring debt sustainability. The renegotiation would secure “substantial debt relief,” to be applied “for the benefit of the country and its population.” The concept of “substantial relief” is technical but, in plain terms, points to the need to reduce the financial burden of the debt, which can be achieved through various mechanisms, including reductions or haircuts.

The Rationale for Renegotiation: Three Criticisms

In general terms, the official announcement clearly conveyed the purposes of the renegotiation. With respect to its reasoned justification, however, three aspects are open to criticism.

The first criticism is that the announcement referred to the “formal launch of an orderly and comprehensive restructuring process of the external public debt of the Republic and PDVSA.” The phrasing is misleading: looking only at General License No. 58, the reality is that neither the Republic nor PDVSA may renegotiate the debt — if by that we mean negotiations with creditors to modify the terms of pecuniary obligations — in accordance with Article 100 of the Organic Law of Financial Administration of the Public Sector, read together with paragraphs 33 and 34 of Article 3 of Regulation No. 2.

The second criticism — which has more to do with communications policy — is that the English-language communiqué contains different information from the Spanish-language one. The reasoned justification for Step Zero of the renegotiation procedure should be a single set of reasons, regardless of the language in which they are expressed. The differences are not minor: the English-language communiqué reports something that the Spanish version omits — the preparation of macroeconomic studies and debt-sustainability analyses. From the standpoint of the transparency principle, that omission is inconvenient.

Finally, the third criticism of the reasoned justification is the statement that the “capacity and willingness to meet our financial commitments were impaired beginning in 2017 as a result of financial sanctions.”

This is a highly debatable conclusion that should follow from the evidence, not from a political narrative. Without denying the regulatory barriers that economic sanctions impose on debt management, the evidenceshows that by 2017, Venezuela had already lost market access because the debt was unsustainable. Backing this analysis, I have explained that the unsustainable indebtedness was, to a significant degree, a consequence of the dismantling of the rule of law. The opposite view has also been defended, emphasizing the impact of economic sanctions. Hence, the importance of an objective and impartial diagnosis of the institutional causes of the debt crisis — not only for purposes of memory and accountability, but also to ensure that the renegotiation addresses those institutional causes and thus prevents new crises.

This third criticism points to an omission in the communiqué that, sooner rather than later, will have to be corrected: any debt renegotiation must start from a diagnosis of the institutional and economic causes that led to the accumulation of an external public debt that could exceed one hundred and seventy billion U.S. dollars (USD 170 billion). If the institutional causes that produced that unsustainable debt are not corrected, every new debt risk ends the same way.

The “Step Zero” Procedure

The English-language communiqué sets out four principles for the renegotiation. The first two — sustainability and comprehensiveness — have already been examined. The other two, relating to the Step Zero procedure, deserve attention.

The first principle of the Step Zero procedure is transparency, linked to good faith. One of the aspects of public debt that has changed most since Venezuela went into default is precisely its transparency, which has received particular attention from the International Monetary Fund.

In any event, as I have explained here, transparency is much more than a good practice: it is a constitutional principle deriving, among others, from Articles 141, 311, and 312 of the Constitution, and is also connected to the international commitments embodied in the Inter-American Democratic Charter.

Accordingly, the Step Zero procedure, designed to carry out the preparatory actions for a potential debt renegotiation under General License No. 58, must comply with the principles of transparency and citizen participation.

This procedure is also governed by the principle of expeditiousness (celeridad), as stated in the English-language communiqué. That principle, however, can be a double-edged sword.

On the one hand, the preparatory phase of the renegotiation, like any administrative procedure, should be guided by the principles of expeditiousness, effectiveness, efficiency, and transparency. But, at the same time, expeditiousness cannot justify actions that, however urgent, undermine the principle of transparency.

Transparency, understood in this way, is not a mere procedural principle: it is a guarantee that creates the conditions for raising the quality of the renegotiation procedure. If urgency turns into haste, the risk increases not only of breaches of the transparency principle but also of preparatory decisions that, because of their poor quality, compromise the process’s outcome.

The renegotiation, as the Spanish-language communiqué states, must “secure the future for coming generations.” That ambitious aim requires raising the quality of the preparatory actions, which contradicts the pretension of an abbreviated or expedited procedure, all the more so given the institutional and economic complexities of the Venezuelan debt, explained here.

The Transparency Principle in the Current Institutional Context

The principal challenge to the transparency principle in this Step Zero is Venezuela’s institutional context, marked by two conditions: state fragility and a weak rule of law. The principal evidence of those conditions is Venezuela’s repeated inclusion in the International Monetary Fund’s Fragile States program.

Part of the initial debate in Venezuela on the announcement has been precisely about the absence of institutional conditions for the renegotiation. Some argue that those conditions must first be created and only then should the renegotiation proceed. Others maintain that perfect conditions do not exist and that the process should begin even under current conditions.

My position lies between the two. Given that the relationship between state capacity and development is one of coevolution, I believe that Step Zero of the renegotiation can begin even under the precarious institutional conditions that currently exist, to the extent that this step contributes to building institutional capacity and to restoring the rule of law. This is what I have termed bottom-up restoration of the rule of law.

It makes little sense to wait for ideal institutional conditions before taking Step Zero, because without that step, it will be difficult to build those capacities. The May 13 announcement may therefore be read in a broader context: the construction of institutional capacities to advance in the economic reconstruction and the restoration of the rule of law.

This approach, moreover, justifies Step Zero and General License No. 58 within the framework of U.S. policy toward Venezuela. Through this lens, preparatory actions — including macroeconomic studies and debt-reconciliation work — can allow public debt to cease being a burden and become an opportunity to leverage growth, particularly by reinforcing the role of creditors and, more generally, private investment.

For Step Zero to contribute to building institutional capacity, it is important to have the support of international organizations, especially the International Monetary Fund, which, for the moment, is not involved in the announcement of the renegotiation.

Institutional fragility undermines confidence in the macroeconomic information that may be produced in this Step Zero and raises coordination costs. The Fund can help build confidence and address coordination problems, particularly as part of a capacity-rebuilding program to produce high-quality statistical information.

According to the United Nations, transparency is a fundamental principle of debt restructuring that enhances its legitimacy. In Venezuela, transparency is among the essential mandatory principles that, according to Articles 141, 311, and 312 of the Constitution, must govern the debt renegotiation process. A final caveat. While advancing in Step Zero amid institutional fragility may be advisable, it is essential to consider the risks fragility entails, particularly to the integrity of the renegotiation. This brings me back to the expeditiousness principle: attempting to advance the renegotiation beyond present institutional capacities and beyond constitutional and democratic legitimacy would further aggravate the problems associated with the public debt, as Venezuela’s recent experience shows.